DOMINION BOULEVARD CORRIDOR STUDY | Chesapeake, Virginia

24 | Market Study

Market Study | 25

Retail

The market appears to have stabilized.

Vacancy rates continue to drop and as of

2014- Q1 were at 6.5%, and rents have

remained stable at approximately $13/

net net net (nnn) average rate. There was

limited construction during the downturn,

which, in turn, has allowed the market to

recover relatively quickly. Retail growth is

tied to household growth, so as the region

continues to gain households, retail will grow

as well.

Currently, the retail market, as defined by

a 10-mile radius around the Study Area,

is mostly in balance relative to demand,

and includes many active retail areas that

provide high amenity benefit for nearby

residents and employees. The area,

which includes a Walmart store, captures

Long-term, the growth in Professional and

Business Services and Health Services as

well as other office-oriented employment will

help bolster the office market.

The office market in the VA Beach MSA

has only recently begun to recover from

a dramatic contraction from 2008 through

2011. From 2006 to 2013, the average

annual office absorption was only half

the volume of office space delivered in

the MSA. Construction activity dipped to

150,000 square feet in 2012 (less than 10%

of the highest annual completion levels

before the downturn). Net absorption was

close to -500,000 square feet in 2011. The

market appears to be improving, showing

a promising uptick in both absorption,

completions, occupancy, and rent growth in

2013. See Figure 12.

Industrial

The Hampton Roads region is unique in that

it has almost double the amount of industrial

space (96M SF) than office space (48M SF).

The industrial market is performing relatively

significant spending from outside residents

for general merchandise, electronics,

and apparel products. Although there are

multiple grocery stores in the north and east

half of the retail area, there exists an under

supply of food and beverage, health and

personal care retail. It is estimated that $22

million in annual sales of food and beverage

are spent outside of the area due to a lack

of large-scale grocery stores in the southern

side of Dominion Boulevard.

Office

The office market is still in recovery, but

2014 is expected to be better than 2013,

suggesting the office market will soon be

in recovery as well. Vacancy rates as of

2014-Q1 were 11.5%, and average rents

at $16.44/square foot (SF), below the

peak of $18.41/SF. Office growth is tied

to employment growth, and 2013 was

challenged by sequestration which impacted

defense and government contracting

companies in the region.

Exhibit II-7

PERCENT NEW HOME SALES BY YEAR

HAMPTON ROADS AREA

2000-2013

Year

% New

2000

30.0%

2001

35.0%

2002

31.0%

2003

29.0%

2004

34.0%

2005

32.0%

2006

30.0%

2007

26.0%

2008

22.8%

2009

17.8%

2010

16.9%

2011

15.6%

2012

16.7%

2013

15.3%

% NEW HOME SALES

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

15,000

20,000

25,000

30,000

35,000

SOURCE: Residential DataBank (2000-2011), Old Dominion University (2012-2013)

0.0%

5.0%

10.0%

0

5,000

10,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Resales

New Sales

% New

Exhibit II-7

E4-11982.40

Printed: 3/27/2014

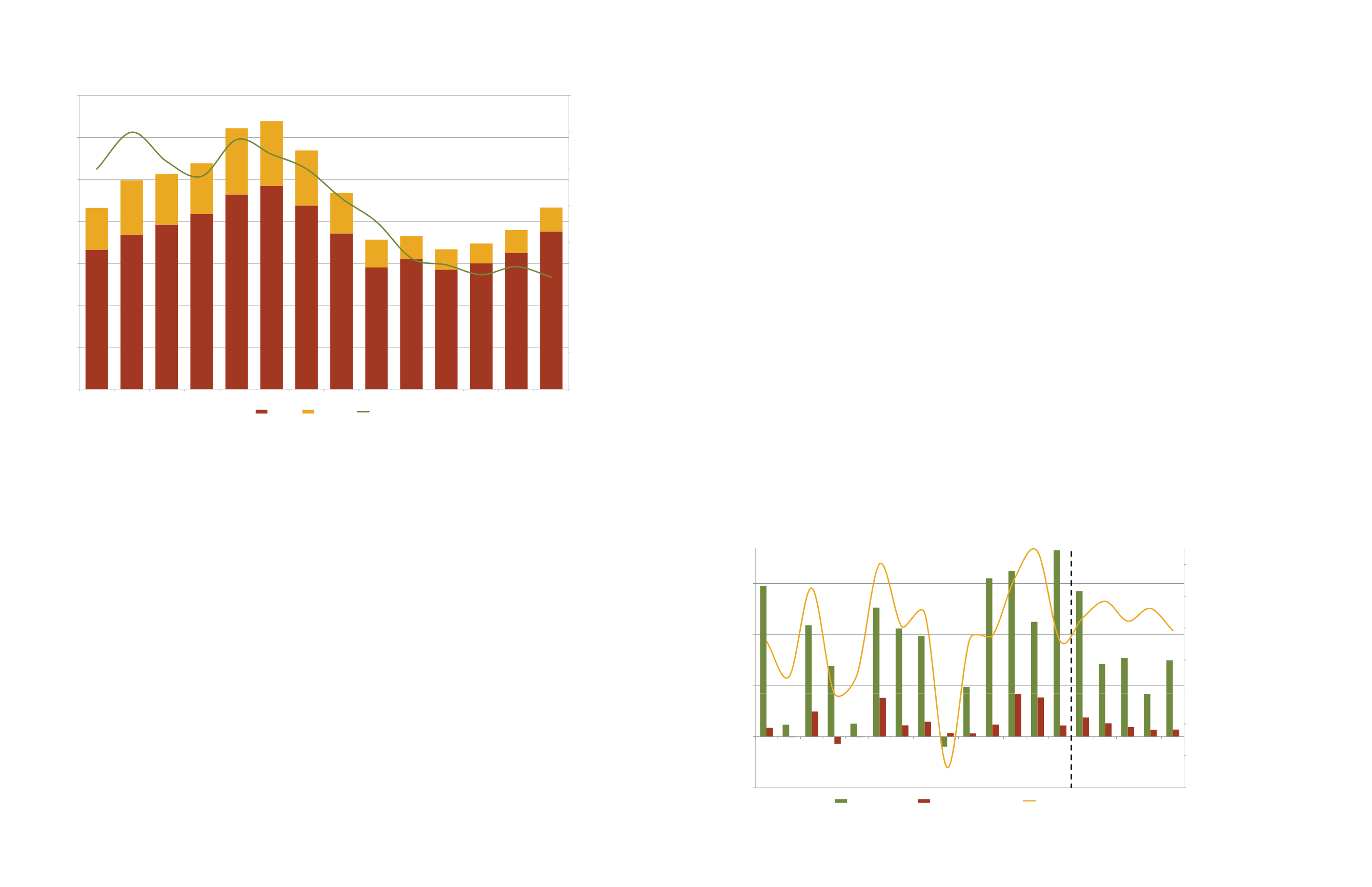

Figure 10: New and Resale Homes by Year,

Hampton Roads Areal 2 0-2013

Source: Residential DataBank (2000-2011),

Old Dominion University (2012-2013)

Figure 11: Apartment

Submarket Absorption

Capture, Chesapeake

and Norfolk/Hampton

Roads Region; 2000-

2013 Source: Reis

well with only 8% vacancy rates and rental

rates close to $5/nnn SF. The challenge

for future industrial is that the types of

jobs that lead to industrial development

(Manufacturing, Trade) are expected to

decrease. Manufacturing is expected to

increase after the large losses from 2001-

2010, but Trade, Transportation, and Utilities

is expected to decrease for the foreseeable

future. Opportunities in industrial are tied

to the obsolescence of old buildings, and

finding niche opportunities.

At the MSA level, the industrial market had

a challenging 2013 after a brief recovery

from the recession. Average industrial rents

and occupancy appeared to bottom in 2010,

at $4.50 and 90%. The market delivered a

total of over a million square feet of industrial

space over the two years, allowing rent and

vacancy to recover to nearly 2007/2008

levels. Vacancy has continued to drop from

the high in 2009. In 2013, however, the MSA

experienced net negative absorption. Rents

have slipped slightly from $4.90 in 2010

down to $4.60 in 2013.

Exhibit III-5

CHESAPEAKE SUBMARKET CAPTURE OF NORFOK-HAMPTON ROADS APARTMENT ABSORPTION

CHESAPEAKE AND NORFOLK-HAMPTON ROADS REGION

2000-2018

-10%

0%

10%

20%

30%

40%

500

1,000

1,500

2,000

PROJECTED

2000-2013 AVG. CAPTURE:

9%

SOURCE: REIS

-40%

-30%

-20%

-500

0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Metro Absorption

Chesapeake Absorption

% Capture of Region

Exhibit III-5

E4-11982.40

Printed: 3/27/2014

CITY OF CHESAPEAKE